As I’ve written before, this newsletter is like a public notebook for me: a place where I jot down my ideas (and non-ideas) to organize my thoughts, expose blind spots, and sharpen weak or incomplete arguments. I write up far more stocks than I own, since I’m a concentrated investor. These writeups stem from my daily hunt for ridiculously cheap, off-the-map stocks, where something catches my eye for some reason.

With value principles hammered into my head since my induction to the investment game, my priority and fiduciary duty is always to assess the downside first. Although I try to scour every stock out there, this downside-focused process often tilts me toward special situations investing.

Let me be clear: special situations investing isn’t inherently better than other types of investing. However, I often find that:

- You’re more likely to unearth market mispricings, and

- those mispricings are often easier to frame in a risk/reward proposition

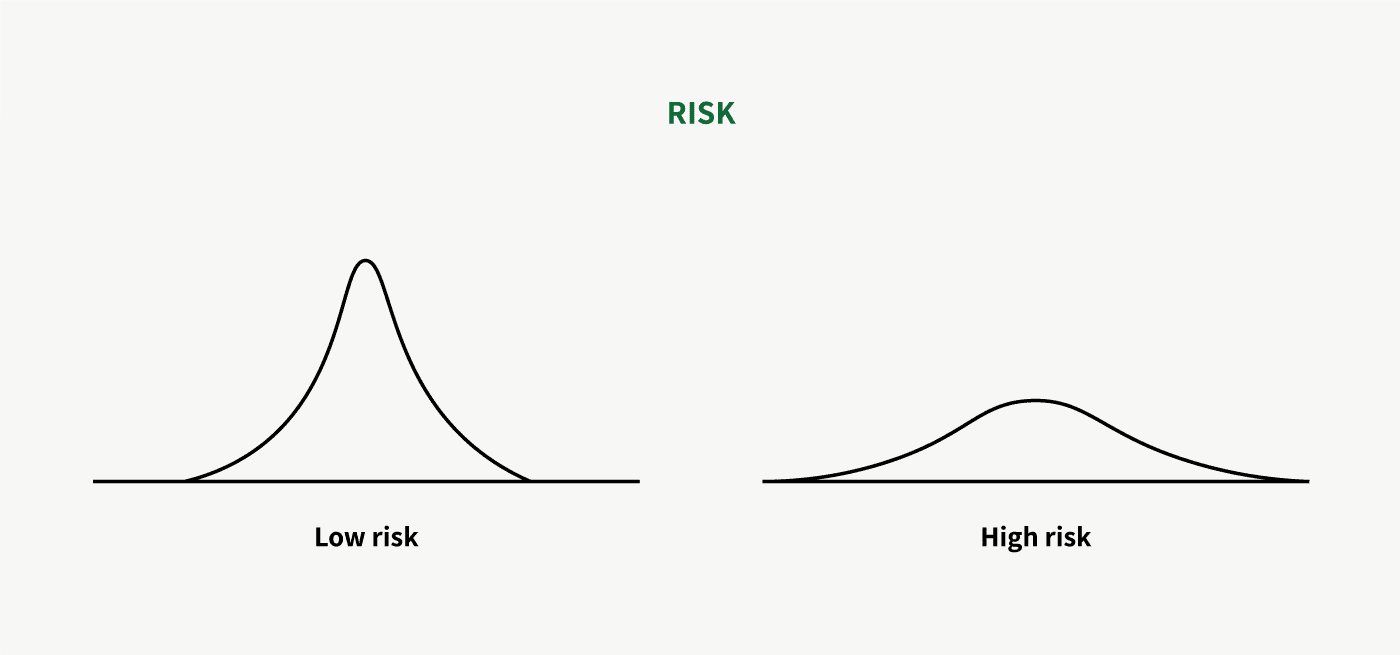

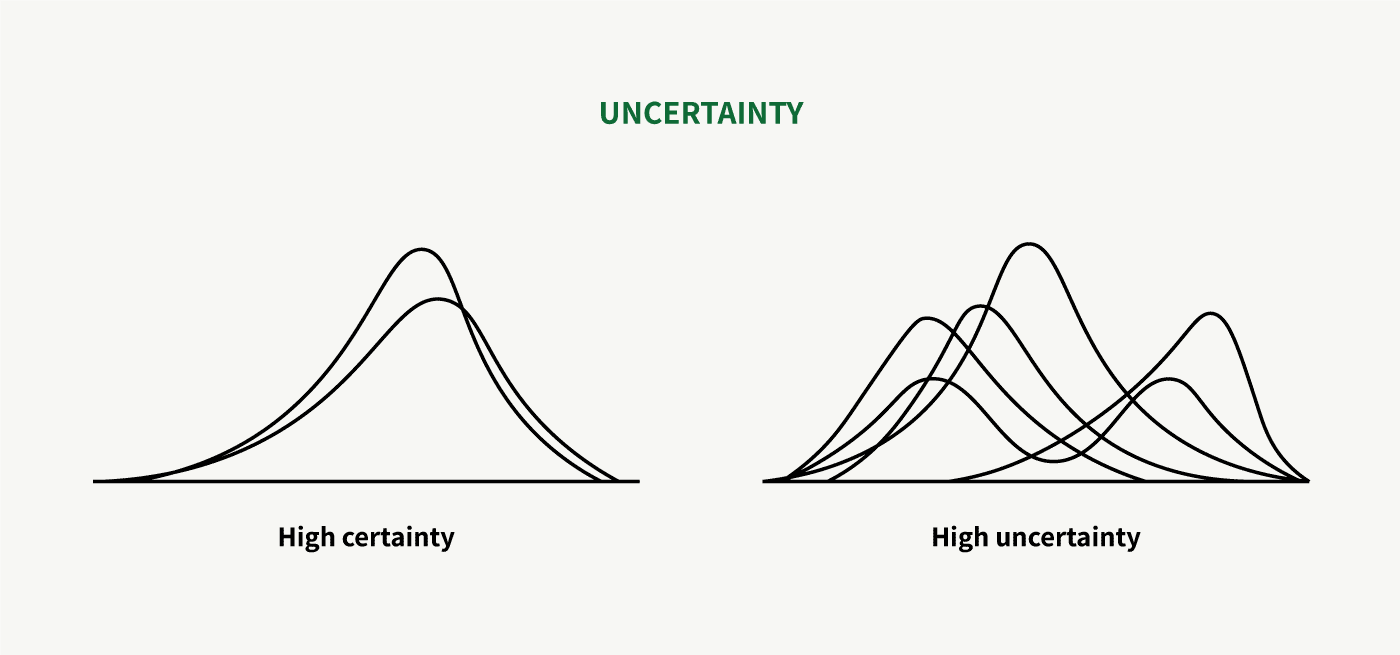

In any investment, what you’re looking for is predictability. And I don’t necessarily mean in terms of cash flows. I mean predictability in terms of the risk — the probability distribution of outcomes. Risk can be managed through position sizing, whereas uncertainty can’t. Risk is when you know the shape of the probability distribution; uncertainty is when you don’t.

Special situations, or what Buffett would call “workouts” during his partnership years, are a lucrative pursuit because they carry relatively low uncertainty, irrespective of their levels of risk. Your potential return may often be capped, but it can be highly attractive on an annualized basis (with the downside being that you need to have a continuous stream of ideas) and you can easily see the risk in front of you, allowing you to size your bet accordingly (using the Kelly criterion).

Secondly, some special situations deliver what insiders call “absolute returns”, marching to their own beat, not the market’s.

The special situation we’ll discuss today offers a ~20% IRR, ± the risks we’ll try to spell out. While this may not thrill those chasing recent market exuberance, I believe the range of outcomes here is narrow, making this return compelling compared to other opportunities out there. (Last October, Goldman Sachs projected the S&P 500 could return just 3% per year over the next decade, or ~1% after inflation.) The situation here is a planned orderly liquidation, and the company is liquid, with an average $10-12mn trading hands daily.

The company’s name is…

Elme Communities, a $1.5bn market cap residential REIT with apartment communities (and one office property) in Washington, DC, Maryland, and Atlanta, GA. The case is simple: despite a decade-long transformation — streamlining its portfolio from four asset classes to one, revamping its operating model, and bringing all property management in-house — Elme has struggled to earn its cost of capital and, more recently, to turn a profit. Short on solutions, on February 13, 2025, the company announced a formal review to evaluate strategic alternatives. The board engaged >80 potential counterparties — pension funds, insurers, institutional investors, financial sponsors, multifamily managers, sovereign wealth funds, family offices, and other REITs — to chart a path forward. Hopes were high.

Two days ago, on August 6, the verdict landed in shareholders’ laps: the company is liquidating. While this may have stung those holding since 2020, watching their investment wane over five years as markets ripped, the board did provide consolation in announcing that it’d already found a buyer willing to take off 19 of Elme’s 29 property assets, with Elme giving itself an estimated 12 months to offload the rest and give the money back to shareholders.

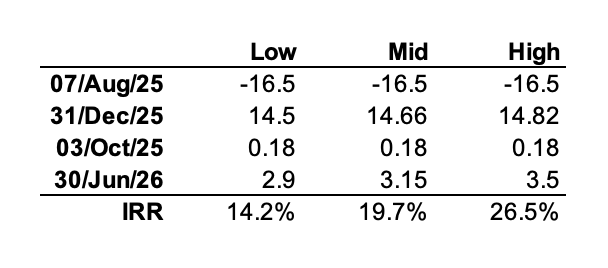

The price of those 19 property assets rings $1.6bn (Elme’s EV is $2.2bn), and the buyer is Cortland, an Atlanta-based multi-family real estate developer and management company. The deal, subject to shareholder approval (a definite proxy statement is on its way), is expected to close in Q42025. Proceeds will be used to pay off all outstanding debt, while securing a new debt facility from Goldman Sachs to fund remaining obligations post-sale. Elme expects to pay an initial special liquidation dividend of $14.50–$14.82 per share after transaction costs. The sale leaves Elme with ten property assets — nine apartment communities and one office property in Washington, DC — expected to be sold within 12 months, yielding a final $2.9–$3.5 per share liquidation dividend at wind-down. This follows an already established regular quarterly dividend of $0.18 per share, payable on October 3, 2025.

In total, Elme will dish out $17.58–$18.50 per share, then vanish. You’re paying $16.50 per share for Elme today. Many might scoff at a 9.3% spread, but the point is that by Q4 this year, you’d recoup 89% of your investment, with the rest arriving later, delivering the following IRR (assuming a final distribution on June 30, 2026):

It goes without saying that liquidations aren’t risk-free and come with caveats. A liquidation could be time-consuming and disruptive, diverting management and board attention from operations, hampering the ability to attract and retain employees and customers, exposing the company to litigation, and/or triggering unforeseen expenses tied to equity compensation, severance pay, and legal, accounting, and financial advisory fees. During the Q22025 earnings call, alongside the liquidation announcement, Elme emphasized the board’s prudence in accounting for all contingencies, including various provisions, in its liquidation projections. For now, we can only take their word, as a definitive analysis awaits the proxy statement.

There are other risks too. A prolonged wind-down could pile up overhead and maintenance costs. Macro factors like inflation and interest rates could upend assumptions for an orderly process. Misaligned management might prioritize speed over value, opting for quick sales to wrap up at shareholders’ expense. The Cortland deal still needs shareholder approval.

On those cheery words, here’s the flipside: Elme’s structured liquidation and open process curb the odds of a sloppy fire sale. A well-executed plan could also act as upside risk for all of the above if it runs smoother than expected. Management didn’t need to give itself a leisurely 12-month (non-binding) window — a long time to sell residential properties with 95% occupancy — to offload the remainder. Executive Chairman Paul McDermott, with a base pay, benefits, and cash bonus of ~$1.9mn but holding over five times that in shares and likely in line for a $5.5mn severance package, seems well-aligned:

There’s potential upside in timing, too. While Elme will likely aim to sell all nine apartment communities as a bundle, then Watergate 600 (the office building), it could offload assets sooner or make additional distributions along the way if selling individually proves optimal. This could boost IRR by a couple of percentage points.

With the first 89% of liquidation proceeds secured, assuming the Cortland deal closes (notably, it’s not contingent on Cortland securing financing), let’s consider the value of the remainder.

Lacking granular data on Elme’s individual properties, it’s likely Cortland cherry-picked the best ones. In FY24, Elme generated $153mn in NOI, less $9mn in property management expenses, which we’ll exclude for conservatism. Dividing this into the midpoint of the full estimated liquidation value (excluding the $0.18 per share quarterly dividend) of $1.57bn, plus current net debt of $700mn, yields a $2.27bn EV and an implied cap rate of 6.3% for the full pre-sale portfolio.

Let’s value Watergate 600 (the office property) at a 12% cap rate (for a commercial office building with 82% occupancy). With $12mn in annualized NOI from Q22025, it could be worth $100mn.

Next, the apartment communities. Cortland will acquire 5,794 homes across 19 apartment communities. Dividing that by 9,374 total multifamily homes and using that as a base for NOI, we can estimate Cortland takes something like 62% of total NOI, or $89mn, off Elme’s hands. This leaves $55mn in NOI for the remaining properties, or $43mn excluding Watergate 600. Elme expects to distribute $3.15 per share from the remaining properties, or $273mn total. Subtracting Watergate 600’s $100mn value and adding $520mn of to-be-issued Goldman Sachs debt yields $693mn in implied value for the remaining apartment communities. Thus, we can back into a 6.2% cap rate on the remaining apartment community portfolio and 5.6% on the portfolio sold to Cortland, per the board’s expectations.

Two assets are wild cards: Watergate 600, accounting for 8% of Elme’s rental revenue, and Riverside, comprising 13% of its apartment community homes. The former was acquired in Q22017 for $135mn; we’ve valued it at $100mn today. Elme has never conducted a formal sales process for the property, which could have option value if repositioned for residential use, given its prime Potomac riverfront location in Washington, DC. Valuing it at its 2017 price could add a couple of percentage points to the IRR. Riverside, meanwhile, offers density and development upside for a buyer, potentially justifying a lower cap rate. But this is tempered by Elme’s three Montgomery County, MD assets, hamstrung by rent control and demanding a higher cap rate.

Elme’s apartment communities are affordably priced, mid-market Class B (and some Class A) multifamily homes in metropolitan areas. Class B properties offer value-add potential, and affordability remains a pressing issue across mid-market rent tiers, suggesting rents can grow as newer Class A properties and homeownership costs outpace affordability. But actually, over the past 5- and 10-year periods, Class B rent growth has outpaced Class A in Elme’s markets. This supports the board’s implied cap rate of 6.2%, especially when recent industry deals show that giants like Equity Residential and AvalonBay Communities are snapping up Class A real estate at cap rates of 5% or lower.

Given a 12-month window for a wind-down, you do face interest rate risk and the potential for a rebound in construction starts (which is down nearly 60-70% from its peak in the metro areas of Washington DC and Atlanta), as housing and mortgage undersupply helps sustain demand for quality, affordable rentals. (The national cost of owning a home versus renting a single-family starter home is at a 20-year high.) But with 89% of your outlay returned by year-end, a liquidation bet like this could likely be worth the wait for the rest.